In my 2013 book MEMEnomics, I dedicate an entire chapter to the analysis of the 2008 financial bailout, its shortcomings and the toxic effects it had and will continue to have on the global economy. To get a better understanding of how dangerous and toxic things have gotten today, it’s important to understand the simple, but delicate relationship money must maintain to economic activity. A layman’s statement of this correlation appears in the book and, to my surprise, has been quoted by several financial planners in their newsletters to clients. It also came close to having me thrown out of a conference in Chicago that was organized by the friends of Milton Friedman, the father of Monetarism who popularized the term “Only Money Matters.” These 3 words became the title of another chapter in which I describe the dangers of having a financial sector in an advanced economy decouple from that economy’s measure of productive output. The quote is this:

“Money is to an economy as nutrition is to the human body. When central bankers ignore that relationship by providing more capital that functionally needed, they debase everything capitalism stands for.”

In the fall of 2008, the financial sector was addicted to a gambling problem originated by something called notional assets, which was made worse by the absence of regulation. The growth of this toxic form of finance had thrown the historically delicate relationship between money and productivity way out of balance. This became a phenomenon that threatened to collapse the global economic order. The entire organism called the global economy, was suffering from metabolic syndrome and its major organs were shutting down. As this ravenous beast ran out of money, it came home begging for a bailout from a government whose regulatory institutions had become impotent and its representatives had no capacity to understand what a responsible regulator should do.

A prudent course of action would have been to rebalance the system by forcing the financial sector to go on a diet. In other words, what was needed in 2008 was a downward revision of the value of the banking industry’s assets, what was historically referred to as price discovery after a market crash. This also needed to be coupled with the decision to allow insolvent banks to collapse or be taken into receivership. This would have allowed the economy to organically regenerate, as the detoxification process would have realigned the financial sector back with productive output. The problem was that instead of our government being the good doctor who saw the long term benefit of these painful and necessary choices, it chose the easy way out and granted the addicts everything they asked for.

One might think this was the end of the story that averted disaster, but the bailout was just the tip of the iceberg on the road to the complete debauchery of global financial systems. Enter Ben Bernanke, Chairman of the Federal Reserve during the financial crisis. Bernanke was considered a god sent to the demigods of global finance as he built his entire career on the argument that the Great Depression would have been averted if it weren’t for Fed policies that tightened the money supply. Desperate for a miracle from the most powerful banker in the world, leaders and CEOs alike, embraced this philosophy as their savior. A decade into these unproven grounds of finance and the move seems to be nothing but a long desperate gasp for air. This linear fallacy from the very top became the catalyst that is now destroying monetary policy and the very virtues that money historically stood for.

In the years since the financial crisis, the Fed started printing money out of thin air. Sure, they gave these financial instruments fancy names like Quantitative Easing, asset buybacks, and special credit facilities. The list of clever names was endless, but the truth remained the same. A central bank only has two boring tools at its disposal and they must remain boring due to the critical function they perform, and here they are: 1. Regulating the money supply and 2. Controlling interest rates. But this was Bernanke’s Fed, and he had completely exhausted these tools and backed himself into a corner from which there will be no escape. Interest rates were effectively at zero, and the money supply had long lost any relationship to economic output. Additionally, the hope that the toxic assets the Fed purchased, will become investment grade at some point has greatly faded. But, instead of writing down these assets, the Fed extended their buyback programs into 2014.

Here we are, a decade into these policies and a gigantic tragedy is beginning to unfold in front of our eyes. In addition to keeping a steady, fat-rich diet of low interest, and an unimpeded money supply, global markets and the Fed’s balance sheet are full of over-inflated and non-performing assets. This phenomenon has become common among many advanced economies it matters not who is in charge of their central banks.

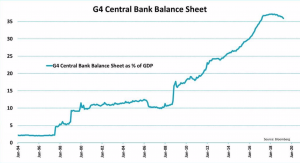

As of April 2019 the central banks of the top 4 economies in the world, the US, EU, England and Japan have a hugely bloated balance sheet that represents an astounding 36% of their countries’ combined annual GDP. This is unprecedented. It is more than 12 times the post WWII historic average. What this essentially means is that the global economy has been living on borrowed time and that the Fed has been in crisis mode since 2008 and must remain in crisis mode for years or maybe decades to come. It has acknowledged defeat and cannot take its foot off the gas pedal. It is a corner from which the only escape is to keep doing the same. It cannot raise interest rates for the fear of crashing stock markets, and it’s unable to sell the toxic assets it has on its books. These holdings are called Mortgage Backed Securities that were at the heart of the 2008 collapse. Today they have grown faster than all the other segments of the Fed’s balance sheet and represent 40% of its holdings, or $1.6 Trillion.

The economies that these 4 central banks represent account for over 55% of the total global output and the bigger these numbers get, the higher equity markets rise on a completely deceptive premise that has little to do with real economic output. It is one big bubble that’s making the global economy increasingly more vulnerable to several contagions. One of these contagions could be an economic slowdown that confirms the systemic failure of this end-stage monetary policy where investors in a panic dump their equity holdings and resort to the safety of cash. The other and more likely catastrophic scenario is if the economy heats up and the Fed decides to raise interest rates to stem the threat of inflation. We witnessed a glimpse of this in 2018 when the Fed raised rates twice and the market lost 5000 points in a few short months.

Whatever wildcards appear, we know one thing for sure, and that is the world’s central bankers have abused every possible tool available to them. Add to that the overvalued toxic assets that caused the 2008 financial crisis which have systemically been legitimized by the world’s central bankers who sanctioned them under different names and repackaged them as legitimate holdings on their books . All these actions have completed the debauchery of money. Today there’s a palpable fear about the precarious state of the global economy and central bankers are quietly beginning to acknowledge their role in getting us there. It’s just a matter of time before the whole house of cards begins to collapse.

Sven Henrich, a leading market strategists and an expert on macroeconomic issues describes the central bankers’ ill advised journey of the last decade and the predicament they’re in today in these terms:

“The capitulation is as complete as it is global and 10 years after the financial crisis there is not a single central bank that has an exit plan. So great is the fear of falling markets and a slowing economy that the grand central bank experiment has ended in utter failure.”

This destiny wasn’t written in 2008. It was born when the Monetarists rose to power along with Reaganomics in the early 1980s. This is when central bankers drank the Kool Aid that sought to make finance an economy on its own. They fully bought into the idea that financial innovation can take money far beyond its historically boring function and made themselves much richer in the process. When the experiment failed in 2008, instead of reversing course, they decided to become even more creative. They manipulated the world’s resources and debauched its financial architecture. They made the poor ten times poorer and the rich 20 times richer and didn’t care about the deep damage they were causing in the long term.

Today, the debasing of a capitalist system based on finance has reached its end state. The tail that has been wagging on a fat-rich diet for the last 4 decades has finally killed the dog. It’s just a matter of when the death certificate will be signed, and who will be brave enough to sign it.